Blog (30)

There just seems no end to the good story: the SA Listed Property Index (J253) recorded a total return of 8.60% in July 2012. The Property Loan Stock Index (J256) and Property Unit Trust Index (J255) recorded returns of 9.12% and 7.46% respectively over the same period. The sector is now approaching R200bn in market capitalization with over 60% of this value comprising only five companies.

As reflected in the graph below, SA Listed Property recorded the highest total return (+8.60%) of the four traditional asset classes for July. SA Bonds (+3.98%) and Equities (+2.71%) were the next best performing asset classes for the month. For the last 12 months SA Listed Property, as an asset class, has recorded the highest total return (35.01%), followed by SA Bonds (17.46%), Equities (14.48%) and Cash (5.71%). For June and July combined, the SA listed property sector has recorded a total return of 16.10%.

Capital Markets firmed significantly during the month with the yield to maturity on the Long Term Government Bond Index ending the month at 6.89% (7.46% - 30th June 2012). The historic 12- month rolled yield of the SA listed property sector moved in the same direction and ended the month firmer at 6.44 % (6.97% - 30th June 2012). As such, the return recorded from SA listed property has been driven mainly by the firming of the capital market yields. Over the last two months the long bond yield to maturity has firmed by 105bps. Comparatively the historic rolled yield of the SA listed property sector has firmed by 102bps.

Important to point out, as Catalyst have mentioned previously, is the ‘other driver’ of the firming in fixed income yields via foreign and local buying of SA bonds. Foreigners have been steadily accumulating SA bonds in readiness for South Africa's inclusion in Citigroup's World Government Bond Index from October. Listed property yields are highly correlated to other fixed income yields. Listed property share prices can both be the beneficiary or victim of capital market volatility. In the short term this impact can be more pronounced.

Catalyst point out that this re-rating (or firming in the SA listed property yield) has driven approximately 15% (out of 16.10% i.e. virtually all) of the SA listed property sectors total return for June and July 2012. The sustainability of this trend is a drum has been beaten for some time by segments of the market.

Supporting the property/long bond yield story: At the July meeting of the Monetary Policy Committee (MPC), the decision was taken to reduce the repo rate by 0.5% to 5%. The committee commented that since the previous meeting of the MPC there have been further indications of an overall slowdown in the global economy, amid the continuing risks posed by the banking and sovereign debt crises in the Eurozone. This negative outlook has contributed to renewed monetary policy easing in a number of countries, including in emerging market economies, in an environment of declining commodity prices and subdued global inflation.

Domestic inflation has continued its downward trend, and is expected to remain within the target range over the forecast period. The year-on-year inflation rate, as measured by the consumer price index (CPI), was 5.5% in June 2012 (down from 5.7% in May).

As at the 31st July 2012 the historic rolled income yield of SA listed property was 6.44%. According to Catalyst, the outlook for distribution growth in 2012 remains reasonable, and the sector is likely to deliver inflationary type growth in income distributions.

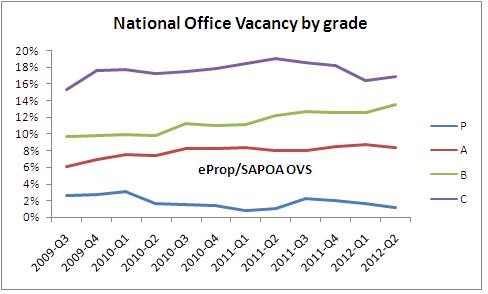

The most recent SAPOA OVS survey as administered by IPD shows that as at Q2 2012, the aggregate national office vacancy rate maintains a modest upward trajectory having now increased over the past six quarters. The q-o-q change represents a further 12bpp increase and a new cycle high of 10.47%. The increase represents a 166 bpp growth on two years ago and a 43bpp increase on a year ago. The trend over the past two years still indicates that the rate of increase has been relatively modest, although the latest increase suggests that office vacancies could remain under pressure and there are no clear signs, economic or otherwise, that this will tapper off in the short term.

At a city level Pretoria and Port Elizabeth (not shown) are moving in a generally downward direction and although Pretoria has seen a fairly big jump, it still is the lowest of all the Metros. Joburg and Cape Town are relatively stable although Joburg is operating at less than 100bpp above that of Cape Town whereas this was substantially higher in the past. Although Cape Town's levels have hardly moved much around the 8% level over the past two years, it is now approaching the 10% mark and given that the survey excludes 'C' grade space this may be cause for concern. Durban's rate has come down marginally but remains the highest overall.

Prime space continues to perform substantially better than lower grade stock with "P" grade offices trending below 2% and "A" Grade below 9%. Negative take up appears to have impacted "B" grade offices the most judging from the trend; and from the fairly volatile trend, C grade space appears to be the subject of refurbishing strategies undertaken by landlords in pursuit of the Prime grade market.

We highly recommend that managers/funds with office assets consider listing their stock on eProp to improve their chances of letting and selling.

The property world and business environment is changing in tandem with macro global forces and micro market nuances. This is just one of a number of themes that eProp picked up at the IPD conference in Cape Town South Africa over 18-19 July 2012.

More...

Natalie Ginsberg had her career sorted, or so she thought at least. With studies and apprenticeship completed, she became one of the senior valuers at the largest auction house in the country, Auction Alliance. However, after Alliance’s recent problems she found herself jobless. But when one door closes another opens:

THE SUBRIME CRISIS, PROPERTY BUBBLE AND THE EXAMPLE OF ICELAND.

Dr. Llewellyn B. Lewis, Principal Consultant, BMI Building Research Strategy Consulting Unit cc says that it is always important to try and make sense of the environment using whatever information comes to hand. Particularly useful are strategic conversations with diverse people of various background, expertise, connections and world views

The past five years have been tough, with the building trades entering a sharp decline from 2007 and then finding themselves in a protected recessionary trough. Confidence of building contractors remain at low levels, with building plans passed, buildings completed and transfer duty paid also remaining near cyclical lows

According to Wall & Smith, there is no doubt that the alleged payment of incentives to banks and others is only the tip of the iceberg in the investigations on the auction alliance business practices by SARS and the EAAB.

Payment of part of the 10% Auctioneers commission to a seller or buyer and the ramifications of how this payment was treated from a tax and accounting perspective by all of the parties involved is something we assume will also form part of SARS investigations.

It is accepted practice that commission, whether paid by either seller or buyer is part of the sale price and will accordingly attract VAT, transfer duty or be treated in one of the ways outlined below.

If the buyer is refunded part of the auctioneer’s commission initially paid by him it is not income, it is a reduction in the purchase price, lower VAT or transfer duty.

If the seller is paid part of the auctioneer’s commission it is not income, it is an increase in the purchase price, higher VAT or transfer duty.

Whether paid to either the seller or the buyer the auctioneer will treat it as a deduction.

It is also important to note if the seller is a non-resident a portion of the purchase price must be withheld in terms of the Revenue Laws Amendment Act No. 32 of 2004 (not applicable to a purchase price less than R 2 000 000)

Source: Wall & Smith

For more information on when VAT or transfer duty are affected see Wall & Smith website

Welcome to the new eProp site Beta version. eProp is the original and definitive commercial property market place serving the SA Real Estate market for the past 10 years with relevant and useful market news and industry information, further supported by unique research, intelligence and insight capacity.

The objective behind eProp’s redevelopment has and will continue to revolve around adding value to you our clients and users. We have totally modernized the look and feel of eProp thereby improving the general user experience; we are also increasing the functionality and tools available to registered users/companies, and are also increasing and improving the offering to advertisers in general. At this stage eProp has news, jobs and property listing/searching sections and over the course of the next few weeks other exciting modules and functionality will be added.

Advertisers and businesses will no doubt find more reason than ever before to engage the eProp opportunity comprising over 25, 000 subscribers/readers/users. We are tremendously excited about taking hands with the property market in SA and look forward to a new mutually beneficial journey together with all our existing loyal clients nurtured over the past 10 years, as well as welcoming new clients and friends into the fold. We are also thrilled about a number of ground-breaking eProp related initiatives within the publishing, employment and broking arena that will capture industry attention. We encourage you to look at some industry testimonials on our new home page regarding eProp.

![]()

eProperty News is a leading online commercial property marketplace serving the Southern African Investment, Office, Retail and Industrial property and allied sectors.