Blog (30)

Economic shift to information age necessitates a review of corporate real estate strategy, positioning and perhaps a debate on the buy/let decision by companies.

Property as an investment asset provides owners with numerous financing options such as mortgage bond, sale and leaseback transactions and getting an equity investor. It does however require huge down payments and cash outflows in the process, which represents an opportunity cost of capital. The cash could be used for furtherance of the business objective.

There is a need for real estate to remain flexible to complement business strategies. Owning may potentially lock an owner long term even where mismatches between property and business objectives arise. Letting does provide companies with some degree of flexibility on lease durations and avoids complexities of financing a property.

Leases however are engineered for profit by the lessor and can be expensive in the long run.

The primary mission of directors is to utilise scarce capital to increase shareholder value and perhaps no one solution exists to corporate real estate with each having pros and cons? Perhaps the type of entity and stage in the life cycle of the business determine what strategy would suit the business?

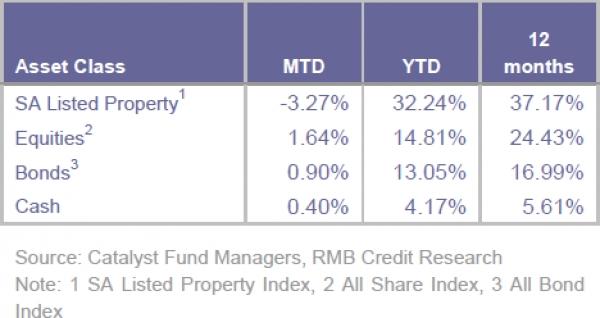

According to Catalyst Fund Managers Report, The SA Listed Property Index (J253) recorded a total return of -3.27% in September 2012. The Property Loan Stock Index (J256) and Property Unit Trust Index (J255) recorded returns of -3.78% and -1.41% respectively over the same period. Capital Markets firmed during the month with the yield to maturity (YTM) on the Long Term Government Bond Index ending the month at 6.86% (6.97% - 31st August 2012). The historic 12 month rolled yield of the SA listed property sector de-rated relative to the 10 year government bond YTM and ended the month weaker at 6.49% (6.20% - 31st August 2012).

For the last 12 months SA Listed Property, as an asset class, has recorded the highest total return (37.71%), followed by SA Equities (24.43%), SA Bonds (16.99%) and Cash (5.61%).

According to Savills UK, Hotel market performance figures showed that the 2012 Olympic Games delivered a gold medal winning performance for the London full-service hotel market as Gross Operating Profit per Available Room (GOPPAR) increased by a staggering 90%, underpinned by Revenue per Available Room (RevPAR) growth of 41%.

After a turbulent June and July which saw market wide RevPAR decline, the phenomenal performance for August, compared to the same month last year, was a timely boost for the London hotel market which, until then, experienced relatively weak revenue growth and no gross operating profit growth over the seven month period to July.Year to date performance (to August) has seen GOPPAR growth of 7% when compared to the same period last year.

Despite some of the negative press and cynicism in the build up to the Olympics regarding reduced levels of demand and over priced hotel rooms over the Olympic period, London hoteliers achieved unprecedented profit growth.

More in-depth analysis shows that the five-star/luxury hotel market and West End hotels were the real winners. Five-star and luxury hotels achieved an incredible 171% increase in GOPPAR in August 2012 over 2011 on the back of class leading growth in RevPAR and Total Revenue per Available Room (TRevPAR) of 64% and 65% respectively (see Graph 1).

Outer London and three-star hotels achieved the lowest GOPPAR growth of all market categories although the level of growth was still impressive at 30%.

The UK's movement back into recession in Q2 12 and the worsening of the Eurozone debt crisis has meant that operating conditions over the first eight months of this year have, on the whole, been challenging.

This, combined with significant increases in supply in the budget and full-service hotel market, has resulted in a significant reduction in growth in TRevPAR and GOPPAR in all hotel market segments. Apart from the respite offered by the Olympics, revenue and profit levels have been relatively fl at since September 2011.

The South African hotel market also needs a boost what with questions raised as to pricing, occupancy and oversupply in the sector. Not withstanding an encouraging growth forecast of 14% plus RevPAR in 2012.

More...

The highly-anticipated SAPOA/IPD South African Biannual Property Indicator to June 2012, spotlights a moderate improvement in the property market over the past six months, but shows little sign of a full-blown recovery across the sector

Anyone involved in the commercial property market, no matter what area, will be aware of the severe risk that rising operating costs have presented to the industry.

Almost in conjunction with the global economy falling apart, and preceded by rolling power cuts, we have witnessed the largest increases in the cost of electricity in SA history. Rates and taxes have also seen significant escalations in recent years, adding to the growing burden on property owners and occupiers,and contributing to the spiraling operating costs bills for commercial buildings.

Commercial property owners have been forced to turn their attention to protecting their valuable income streams as much as possible. It is a testament to the resilience and quality of the industry and South African business as a whole that returns have not suffered to the same extent as those in other parts of the world.

This has not been easy though, and many management teams have worked tirelessly using the best methods available to put in place measures to control, monitor, reduce and compare their costs.

To put this into perspective, average operating costs per square metre grew from R19 in 2005 to R38 in 2011 according to the 2011 IPD Income and Costs Digest. This doubling of total costs equates to annual cost inflation of around 12% a year for the six years to 2011, significantly above CPI over the same period.

Drilling down into individual costs, the main culprit is unsurprisingly electricity, which grew from R4/m2 in 2005 to R12/m2 in 2011. No fancy calculation is needed here: electricity costs have tripled in 6 years, a tremendous adjustment for commercial property owners to absorb. The fact that we enjoyed relatively cheap electricity for years does not make this increase any easier to bear now.

In order to manage these costs effectively and to measure the success one is/is not achieving, the practice of benchmarking has become very relevant. The benchmarking of investment property returns has been around for some time thanks to IPD, but recent emphasis on cost control has led to a demand for a cost benchmarking service.

For this reason IPD has developed and released the first edition of the Income and Costs Digest in 2011, which provides the most accurate and comprehensive picture of the state of operating costs in the commercial property industry.

To find out more contact Chele Moyo: This email address is being protected from spambots. You need JavaScript enabled to view it. or call 011 656 2115

When there are Royal weddings and countries jostle to hold grand sporting events it’s often to distract the people from recessions, wars and scandals. So it’s hard not to be a little cynical about grand gestures by politicians purportedly for the good of the masses. Some would suggest a connection between the ANC youth league’s intention to make Cape Town ungovernable and the latest announcement by the City to spend R132 million on community facilities this municipal financial year

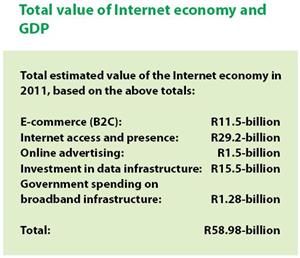

South Africa’s total GDP is approximately R2.964-billion. The Internet economy, as a proportion of GDP, is therefore estimated to make up 2 percent of the South African economy. The result is that an Internet economy, worth R59-billion in 2011, could grow to as much as 2.5 percent of the economy by 2016.

The Internet Economic Impact Study, conducted by World Wide Worx (WWW) shows that at the end of 2011, South Africa had approximately 8.5-million Internet users. This represented no less than a 25 percent increase over the 2010 figure of 6.8-million, maintaining a high growth rate fuelled by the explosion of smartphones in the South African market. Consequently, with the number of Internet users having accelerated from 2008, the number of experienced users will begin accelerating in 2013, and will continue to do so for the following five years.

What is the Internet economy?

The Internet economy comprises access to and use of the Internet, investment in infrastructure and expenditure in Internet activity in a country. These include Internet infrastructure, money spent on online retail and online advertising, and business and Government engagement with the Internet.

The size of the Internet economy is not officially measured in South Africa, and has to be estimated based on a range of available expenditure measures. This is an indication partly of the lack of awareness of the significance of the sector, as well as the lack of maturity of Internet use in business and Government.

Business-to-Consumer (B2C) e-commerce comprises both traditional retail conducted in the online space and intangible products like air ticket sales, fulfilled online.

The total spent on online retail goods in South Africa in 2010 passed the R2-billion mark for the first time, growing by 30 percent to reach R2.028-billion. In 2011, this high growth rate was maintained, with a further 30 percent increase, to R2.636-billion.

More recently advertising for online shoes and fashion has hit mainstream television advertising which is an indication of the threat to traditional retail and the anticipated boon for warehousing and logistics.

The following figure from the report shows the Rand value of online retail each year since 1996 (it excludes travel, which is not traditionally classified as retail. However, online retail is dwarfed by the sale of air tickets online which have come close to the R9-billion mark, growing by 24 percent in 2011, suggesting it will pass the R10-billion level in 2012):

According to WWW's Goldstruck, SA is entering what he terms “the golden era” in which the build out of Internet infrastructure will reach a peak in the next few years.

The number of Internet users in SA is also expected to rapidly increase, stimulated in part by the smartphone explosion. World Wide Worx estimates true individual mobile penetration to be at about 80%, with 40 million South Africans using phones.

“These users represent the future potential of Internet growth in SA. Around 10 million phones are sold in SA every year, and it is expected that by 2013, smartphones will account for half of this number,” says Goldstuck. “Since smartphone users eventually become Internet users, we can expect the Internet user base to grow at an accelerated pace.”

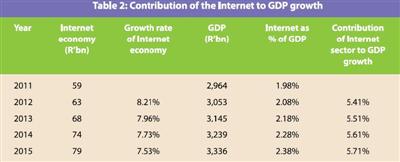

The South African Internet economy is expected to grow to 2.5% (or R79 billion) of the GDP by 2016. “Looked at in another way, it is likely that over the next five years, the Internet economy will begin approaching the size of the construction sector – an estimated R120 billion in 2011, suggesting this is potentially one of the new building blocks of the South African economy,” says Goldstuck.

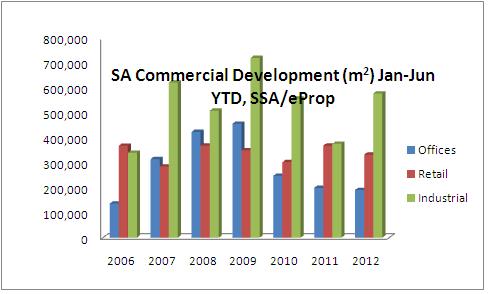

Coming off the heady heights around 2008, commercial development activity now appears to be emerging from it's trough encountered around 2010/11 and where all segments of the sector had bottomed, as reflected in the graphs below. At constant prices, commercial investment activity is up by 8.2% (as compared to -1.4% for residential); it is virtually flat for the value of commercial plans passed.

Midway through 2012 (Jan-June YTD as measured in physical space, m2) we see that the trend in planning activity has picked up; so too for completions and particularly regarding industrial investments: Retail planning activity is up just over 8%, with industrial up 26%; in terms of completions retail is down nearly 10% and industrial is up a hefty 53%; both office planning and completions are down.

At a Provincial level, the Western Cape is showing robust confidence with planing activity strongly positive for all segments, so too Limpopo albeit of a lower base; Industrial planning is very strong in KZN at over 57% or 223,000m2; by comparison Gauteng industrial planning is down. On the completions front, Western Cape Industrial is strong at over 115%, or over 163,000m2; Eastern Cape and North West office completion activity is strong as is Free State retail; Gauteng is showing positive growth for all segment completions - particularly strong for industrial at 62% or over 264,000m2.

The reasonable investment returns offered by real estate coupled with appetite for the asset class (both direct and listed), is no doubt driving the relatively good growth in commercial investment activity, but in order for returns to be sustainable, it remains incumbent on market fundamentals to help prop up demand.

![]()

eProperty News is a leading online commercial property marketplace serving the Southern African Investment, Office, Retail and Industrial property and allied sectors.