Residential property market slowly moves into its super-cycle “correction”

John Loos, Household and Property Sector Strategist at FNB observes 'a tougher year for residendial mortgage lending ahead, as the residential property market slowly moves into its super-cycle “Correction”.'

John Loos says best tread carefully in volatile times as prime rate rise to 10.25%

The Reserve bank (SARB) Monetary Policy Committee (MPC) decided today to hike its policy Repo Rate by a further 50 basis points to 6.75%, a move that will see Commercial Banks raise their Prime rates to 10.25%.

House prices a signal of gloom

The trouble with house prices is because of a booming market that causes consequence of upbeat consumer confidence.

2015 average house price growth was slightly slower than that of 2014 as a whole

In December 2015, the FNB House Price Index inflation rate continued its mild year-on-year growth uptick of recent months.

Current increasingly severe financial constraints in South Africa could lead to a refocus on home ownership

The pressure that for some two years now has been felt by the South African consumer, although regrettable, could be having a beneficial effect in one respect.

So South Africa’s “Big Issue” has very much to do with economic growth, or lack thereof

Economically, we are likely in the early stages of what I call the “stagnation” or “correction” phase of the economic super-cycle, “early” meaning perhaps 4-8 years in (depending on whether you ignore the short growth up-tick around 2010/11 and start the clock in 2008, or otherwise start counting from 2012), and the length of such super-cycle stagnation phases can conceivably roll on for far longer than that.

Nominal sales growth measured 7.3% year-on-year in October 2015

The still-reasonable real growth is in part about reasonable nominal sales growth, which measured 7.3% year-on-year in October, but also still very much about low Retail Price Inflation of 3.9%, contained by a broader benign inflationary environment that currently persists in South Africa.

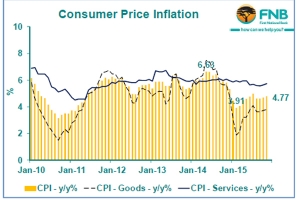

The November CPI inflation rate edged slightly higher, from 4.7% year-on-year in the previous month to 4.8%

The November CPI (Consumer Price Index) inflation rate edged slightly higher, from 4.7% year-on-year in the previous month to 4.8%.

2015 has seen some positive growth, but residential building and fixed investment remains low

2015 has seen some positive growth, but Residential Building and Fixed Investment remains low.

September Retail Sales growth slows, but still solid given the weak economic conditions

Real retail sales growth for September continued to record a reasonably healthy growth rate under the weak economic circumstances.

![]()

eProperty News is a leading online commercial property marketplace serving the Southern African Investment, Office, Retail and Industrial property and allied sectors.