In our last edition, we discussed that the eProp Commercial Property Confidence Index (CPCI) conducted over February/March 2011 and polling industry business expectations for the next six months, reached an aggregate level of 52 in March 2012. This is the first time since March 2008 that the index broke through the neutral 50 mark and speaks to a slight improvement regarding the outlook for the sector overall

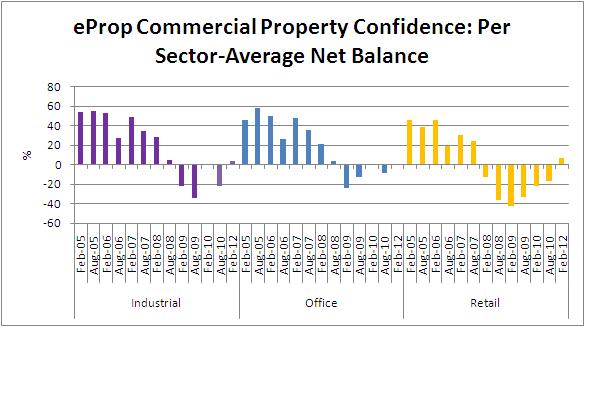

By property sector and on a net-balance basis (spanning a range of +100 to - 100 and where 0 is neutral) the retail property sector has the best outlook (+7), followed closely by industrial (+4) and then offices at 0. For retail the steady path back to a more positive outlook can be clearly seen in the graph below. For offices and industrial the trend is perhaps a little more volatile which speaks to the level of uncertainty belying fundamentals generally and as compared to retail where the sentiment has perhaps been more closely informed by the consumer-based macro economic cycle.

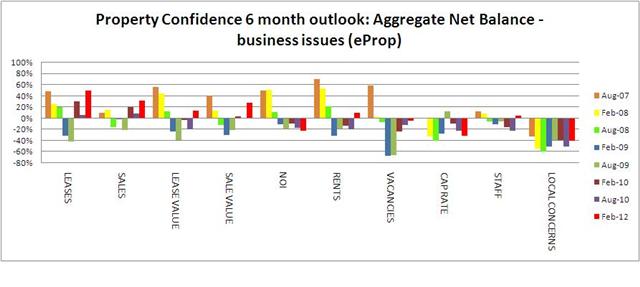

In terms of the business issues contributing to the CPCI index, we see that the more positive outlook is influenced by a firmer expectation around the number of anticipated sales and leases volumes, as well as growth in the values attached to these. Encouragingly, on balance and for the first time in a long time, growth in expected staff complement is slightly positive.

Whilst gross rental value is expected to grow, it is clear by the deterioration in Net Income, that costs remain a major bugbear to the commercial property environment. A deterioration in Cap rates is expected which in turn could account for the more bullish outlook regarding acquisitions. Still representing the biggest concern for the sector, is the net balance of 41% of respondents anticipating that their concerns around local government issues in which their assets are located in, will increase. Presently and over time, it also appears that the concerns in Gauteng are not necessarily worse than for example the Western Cape, though of course this is relative as the comparative level of service is not benchmarked.